I would like to request some support from your side:

Currently running several backtests to simulate behavior during drop in April.

Therefore my concern about “Max Equity Drawdown”

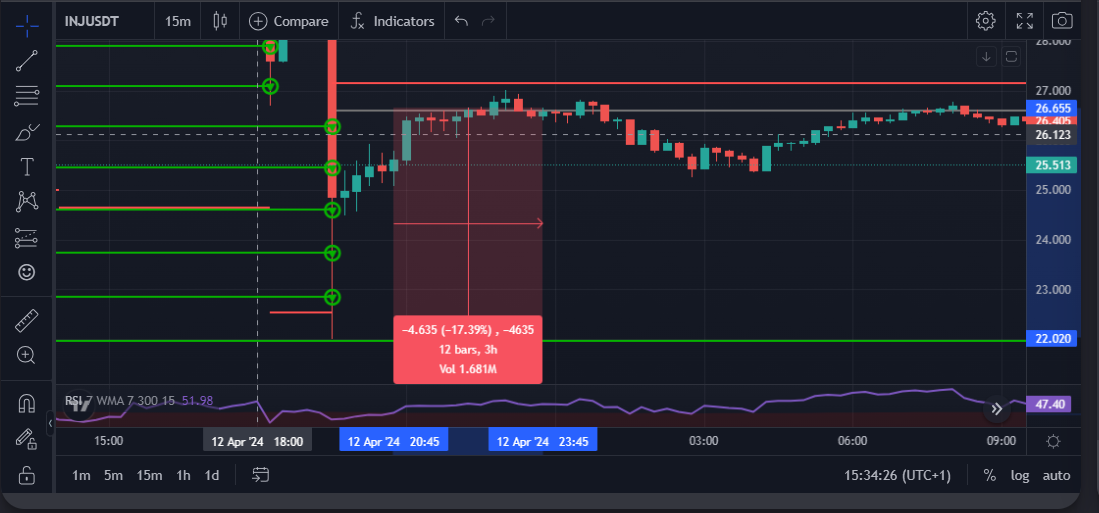

On the results overview : max drawdown -1.32%

However based on the data from trading view at some point when most of the DCA were already used the price went down -17,39% from avarage entry price.

Maybe I’m wrong but it would result [Negative Unrealized Profit] which could potentially lead to liquidation [depends on leverage and account remaining amount ]

From what I understand, the max equity drawdown is calculated from all your available money. So if you haven’t used 100% of the available money to enter a position and haven’t used leverage, the drawdown will be less important than the 17% that you are seeing in trading view. Second point to take into consideration is that when you are DCAing, you are averaging down the whole price of your position, so this means that the drawdown can be less important.

Let me know if this answers your question. See you around!

Hello, Thanks for your reply.

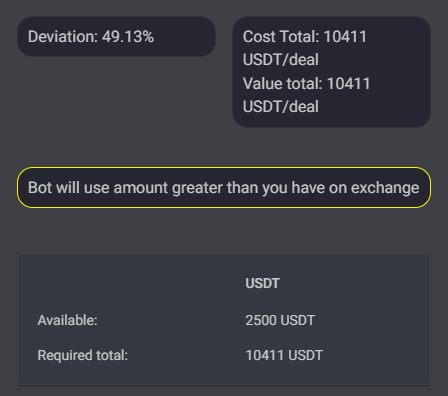

I’m running on test account with 2,5K USDT on it.

The bot set to use 10,4K usdt. Therefore i assume that my account leverage around 4.

So how I can have only -1.32% max equity drawdown.

Just lets do a quick calc:

My bot used 18 DCA, which is 4976$ and price moved down in moment when the market crash in April.

So the unrealized profit was -17,39% [-865$] and then it manage to recover.

Ok, I’m not a Gainium expert but can you share your bot URL to have to try to have a better look at your bot details?

And also I have a question that could maybe explain why you have such a little drawdown. What is your base order quantity? If your base order is 5% of your total or free funds, even with 18 DCA and a 17% crash, you could still only have a -1,32% drawdown from your total funds. (Also even if the bot is set to use 10,4K cause you have a x4 leverage, it doesn’t mean that it will use all the funds, everything depends on the settings).

You should also look into the setting details of the DCA, it is hard to give you an answer with only the information that you are giving.

Lets take another scenario: We will not use leverage to avoid confusion.

Imagine we got trapped with bad entry in HBAR/USDT straight after the pump.

The HBAR dumping down.

The backtest results a pretty close to my calcs in this situation

[My concern that looks like the backtest sometimes is not showing the real drawdown results]

Assume we enter trade on 24 April 06:00 Long

Account size: 2500$

Base Order - 18$

Safety Order - 18$

DCA - 22pcs

Step scale - 1,02

Vol Scale - 1,15

The equity drawdown is not the deal drawdown, you cannot measure it on the chart. The equity drawdown is the distance from the top to the next low in your equity value, which already includes all accumulated profit. So the more profit the strategy makes at the start, the lowest the drawdown will be.