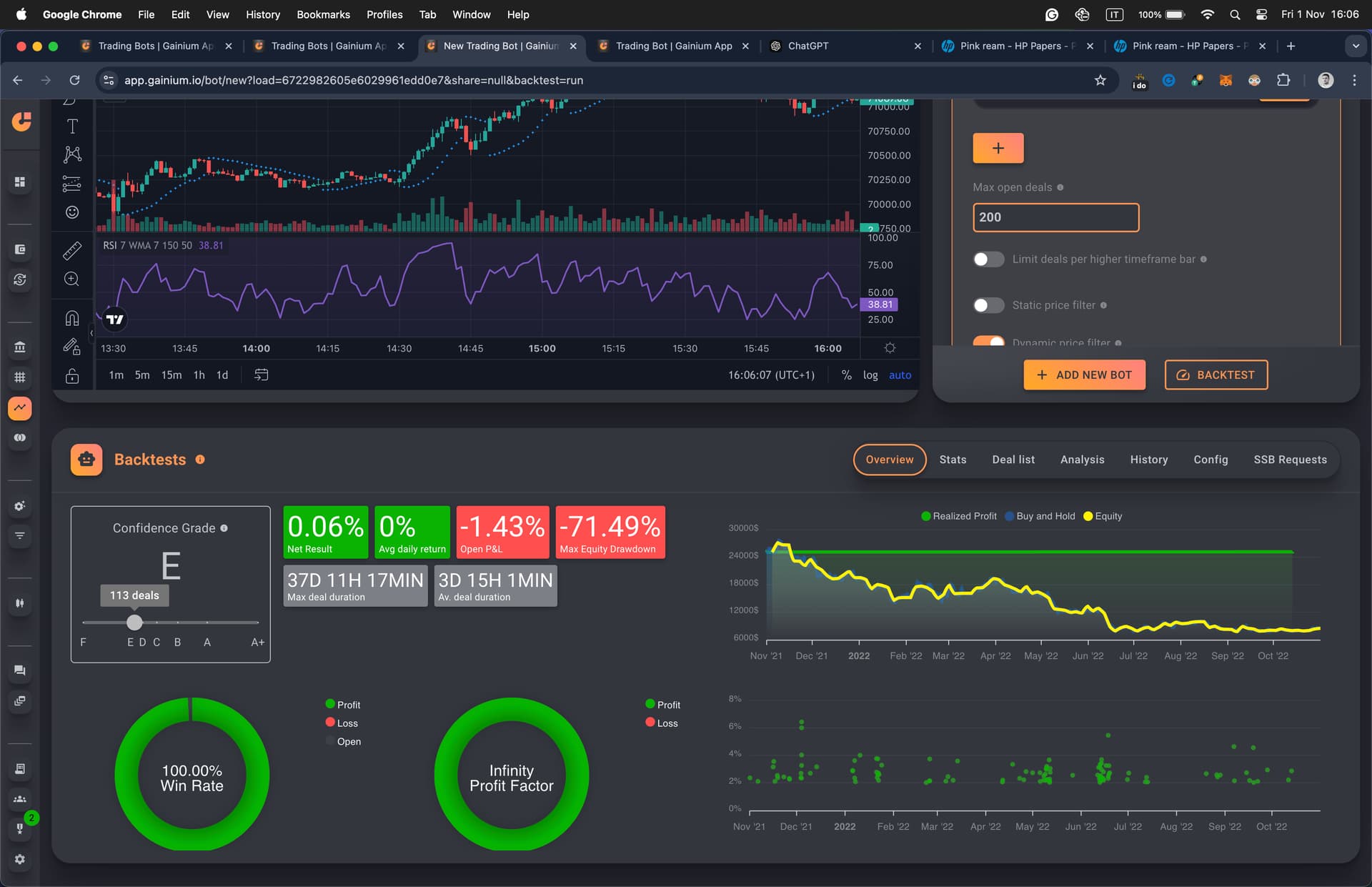

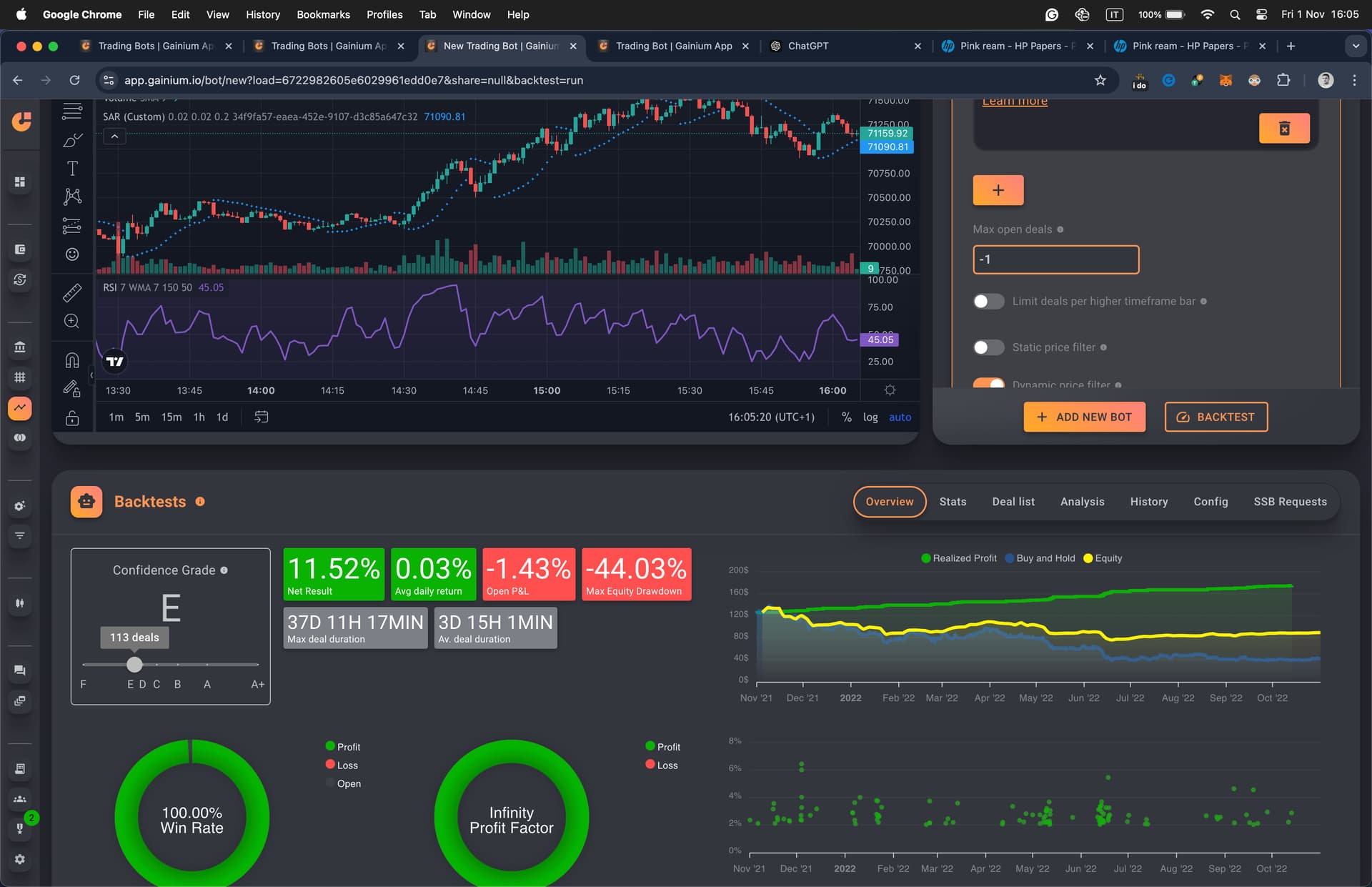

The current calculation of the NET PROFIT % in the backtest is inaccurate mainly because the backtest is based on the max theoretical funds the bot could use after filling all DCA orders, simultaneous deals and multi-pair, which makes the backtest results unrealistic - very respectfully.

The NET PROFIT% should be calculated based only on those funds that were actually used in the trade. How? simple - by tracking the actual funds used for each deal (after the deals are closed) and then calculating the NET PROFIT% based on these totals. This way we will have a more accurate NET PROFIT % not influenced by the max bot allocation

when you look at this backtest comparison between the exact same bot settings we notice the problem: one bot is using -1 and one is using 200 deals (even if the bot never reached that number ever but only 113 deals in total) (Gainium app)