I did a lot of tests imagining a bot that can be run all the time, let’s say which works under all market conditions. So I don’t need to take care of it. It would be a pleasure to take together all the knowhow to maybe create a rocket bot, that is pretty save, with not much drawdown, a good net profit and which works under all market conditions.

Here you see the data from the 4 Year Period from 21.9.2021 - 21.9.2025. So this data should be very reliable running during all different market conditions. Of course I realized that the outcome of the performance is different depending of the beginning date of the testperiod. When the backtest is run, beginning in a bullrun, it’s different than when starting during a bear market.

That’s an important point. You cannot know at what market conditions the bot starts. Therefore you always also consider other scenarios.

Maybe Gainium could even create a set of hand-crafted, preset scenarios with pump, sideways and dump and mixtures of those. If we run our backtests against those instead of our own data, this would help us to compare strategies.

The strategy looks good; it’s clearly a trend-following one, which forces you to enter the trade in the best possible condition to avoid a losing streak (which is inevitable) that could wipe out half your funds. But perhaps it would work even better if you gradually increased your funds. You could also add another indicator to confirm the trend or perhaps one to avoid entering at a potential all-time high (ATH).

Thanks for sharing! Looks good, but in my experience leverage and combo is not a good combination, there are some things the backtest cannot emulate, like the time it takes for a combo to cancel the grid and issue the TP/SL order. I would let it run in paper trade for a while, and you may also consider testing the same period without entry conditions just to see what’s the real impact of the indicator entries.

I now managed to get the Bot Profit to 547% with adjustments

Without entry conditions its generates 140% less! So with this entry condition it seems a good starting point. You know this start condition with HMA50 greater than HMA200 I got from one of your strategy videos

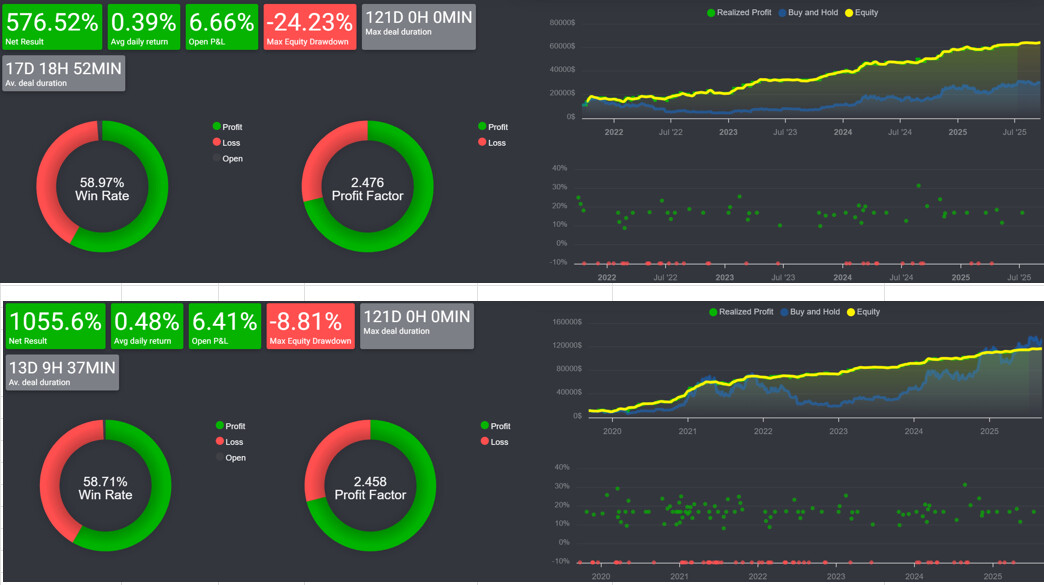

I just made another test. The first picture is with the 4 year testperiod. The second is from July 2019 until September 2025, so over 6 years plus. Why does the test with 6 years plus have much less drawdown with the same adjustments? This huge difference seems very strange to me. Does somebody have an eplanation for this? @aressanch

Hi Oil, there are several indicators that can help you. For example, an overbought RSI on the 1-day timeframe, the ATH created by Gainium, Supertrend on the 1-day timeframe, and even the much-discussed 50-week EMA.

One thing you can do is create a paper bot and see how it performs for at least six months. Another possibility is that if the results are so good, it can produce similar results with other strong currencies.

It’s also possible that the simple strategy will work on its own for a long time.

All the tests we do are based on past performance, but in my experience, the best test is to face it head-on. I look forward to seeing how it goes!

The drawdown is the drop from the top to the bottom of the equity curve/ The backtest that ran longer accumulated more profit, so when both went through the same bear period both experienced a similar drop, but the longer backtest had already accumulated more profit and hence the drop in % was smaller, even though the drop in $ might have been the same for both.

a 60% of win rate is really good and the profit factor of above 2 is excellent, and thats why you must suspect of such good results. You can be overfitting your strategy wich is when you refine too much your strategy values to match the data of the past.

By the way. I realized that Gainium sometimes generates different results when running a test right after importing a .json file, compared to setup a new bot and then inserting the values manually. So if I wanna be sure, the test is correct I do it by manually entering all the values.

Yes it happened to me too. But opening the backtest the results are different. This is new. You can create a Ticket to be investigated by Gainium. Save some screenshots as evidence