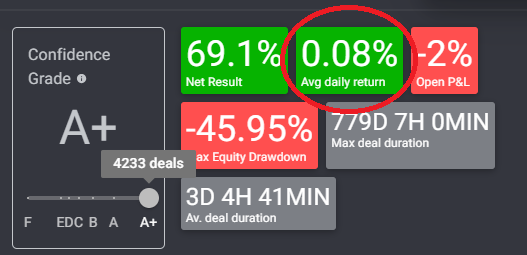

When I backtest a strategy that is supposed to compound, something that could be useful to know is the daily return. The feature suggestion is to change the average daily return by the daily return when using a compound strategy as it is more informative.

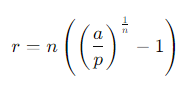

To do that the formula to use is r = n((a/p)^(1/n)-1) or

where

r: daily return

a: total money at the end of the backtesting period

p: total money invested at the beginning of the backtesting period

it has to be an average indication anyway because all deals may no close at the same percentage - It may simply adapt base on the bot settings so if we select compound the stats will show the result including the compound profit

Yes it has to be an average, but the way it’s done now is not correct, I mean dividing the net result by the number of days you backtested a compound strategy, don’t give you the average daily profit, it only gives you “the net result divided by the number of days”. To calculate the average daily profit for a compound strategy, you need the formula above. But yes I agree with you