Hi,

I have a Paper Bot running a couple of days. When I do a backtest of the same period, I get much better results. Can someone Explain how? otherwise I can not relay on backtesting.

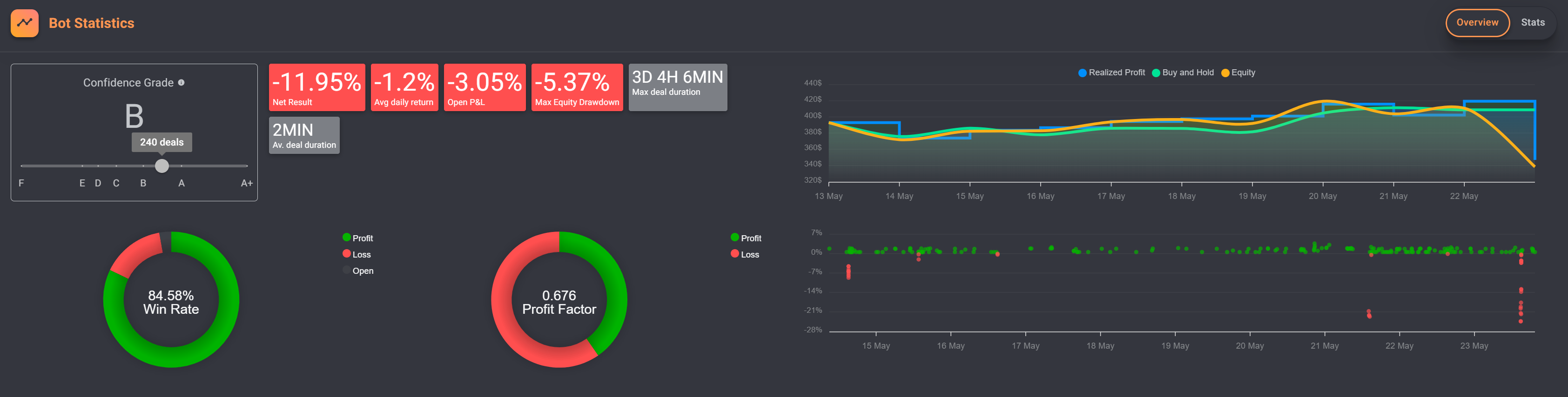

Backtesting Results:

Real Results:

Bot ID: Gainium app

Hi,

I have a Paper Bot running a couple of days. When I do a backtest of the same period, I get much better results. Can someone Explain how? otherwise I can not relay on backtesting.

Backtesting Results:

Real Results:

Bot ID: Gainium app

There are a string of liquidations in the paper bot that didn’t happen in the backtest. We will investigate that.

In any case, I can already tell you that the higher the leverage the more likely that both the backtest and the paper system will differ from live results. At 50x, I can guarantee that it won’t be the same. The backtest and the paper are emulations, emulations contain small differences from live, but these differences are multiplied by the leverage.

If you want better results you would have to test it live on a small budget. But I can also already tell you, you will most likely lose money. No one ever got a fortune by using 50X leverage. You may get lucky once or twice, but do it long enough and you will lose your money many times over.

okay, thanks for clarification. I’ve only tested it on paper and one live bot with very little amount of money but this one performs a bit better.

how much leverage would you use in the bots. My experience last only two month ![]()

To be honest I don’t like to use leverage, but I’ve tried some strategies at 5x. Imagine that at 5x you only need a 25% drop to liquidate the deal (assuming isolated). And 25% in a day is not an uncommon event in crypto.

Isn’t it even less than 20% in isolated mode and without additional margin? And on the exchange you could always add margin to the deal. In cross mode it depends on the order size in comparison to your margin, what the effective leverage is. But all deals share the same margin. Or you create a sub-account, add some funds and start a single deal in cross margin there. That will behave like an isolated deal as well with the difference that you can add margin before starting the deal.

Response from Maksym:

User set up a dynamic filter with extremly low deviation even for 1m chart. In backtester we checked once per candle dynamic filter if start is not ASAP. In case of ASAP, backtester can checked twice per candle: first time on candle processing start if mac deals less than actual deals, second time in checks when deal is closed and ASAP requested new deal to open. Also slippage, in 50x leverage it can lead to significant change of the result, while backtester adjust close deal price to be as close as possible to target %.

I’m not sure that this settings can be properly backtested

Thanks for your reply @aressanch .

As I understand it correct: my strategie is very high risk and the backtest results should have taken with grant of salt…if it is like this I highly recommend to inform the users if someone creates such a strategy. Maybe it can be done with a information box that the strategy created can varry a lot from the actual results otherwise people will get traped.

Thank you