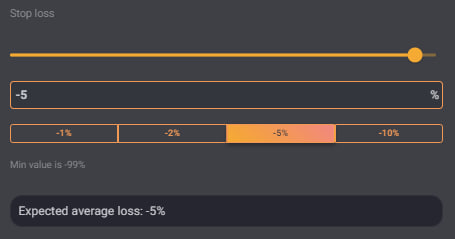

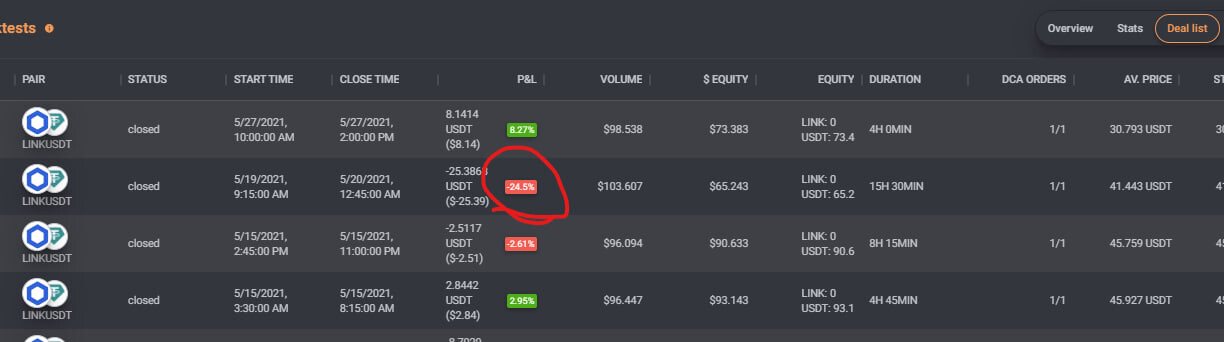

I have a peculiar result and have also noticed this in other backtests… I have deal losses much higher, despite setting stoploss for much lower. Is there something with the stoplosses that is not standard?

Here this bot is 1X and there’s a 24.5% loss despite a -5% stoploss set. The take profit is by indicator.

Thank you for your considered thoughts. Thing is in the backtesting don’t we specify the slippage already. so that should be set? i can see it could be slippage in real life, but with backtesting, shouldn’t any slippage be simulated and in a controlled environment and should not be so high?

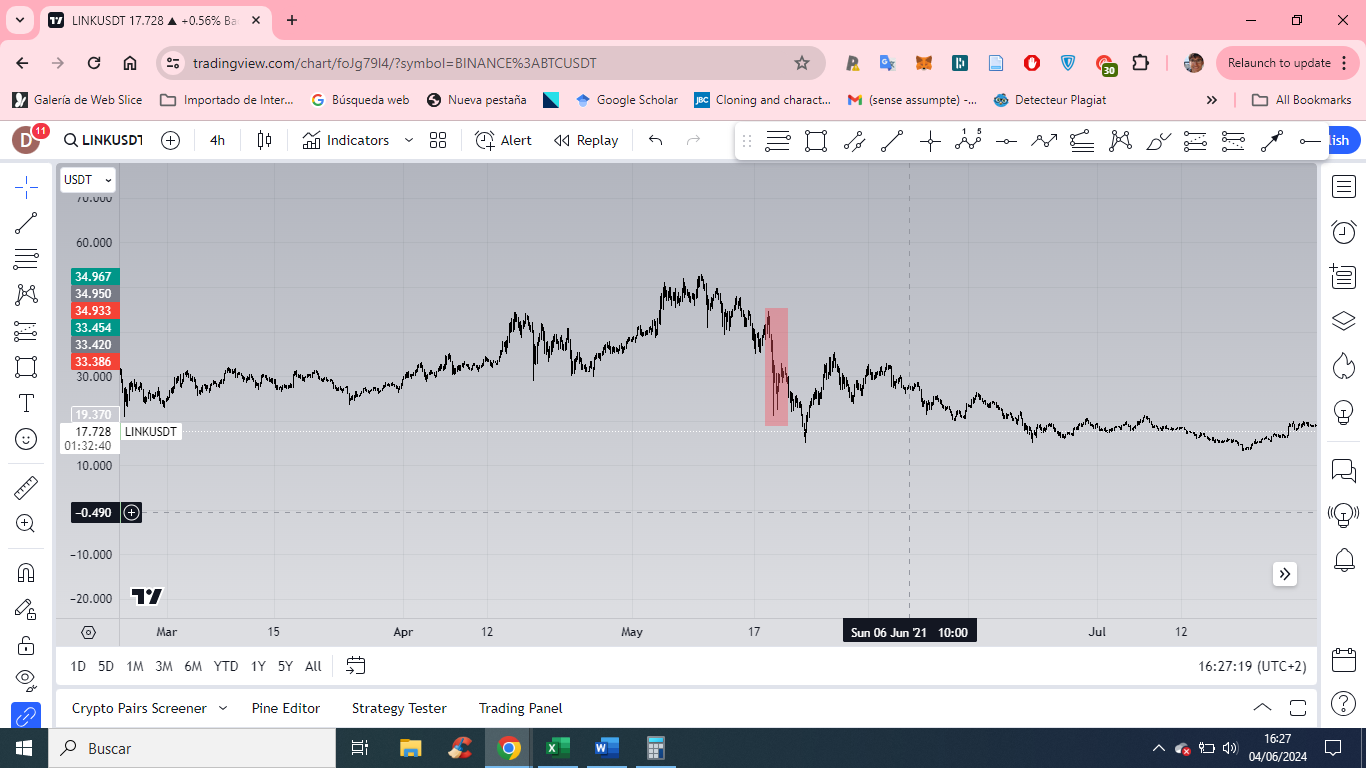

You’re right. I don’t know if it can be due to the speed of the fall, if it’s not that I can’t help you… Maybe Ares or Maksym have an better idea of what it can be.