I’ve been doing some backtesting to compare all the S- strategies from @Rossano.

1. Methods:

I’ve tried to compare the parameters as closely as possible. I always used the same Bybit paper account ($2500) with the default settings presented as Rossano published them in each topic. I tried to backtest for each S strategy the profit currency on base (BTC) and quote (USDT) and for the S6 and S10 I tested the Standard and 0 MOVS strategies.

I tested 4 periods of 3 months each time:

February-March-April 2024

November-December-January 2023-2024

August-September-October 2023

May-June-July 2023

2. Results

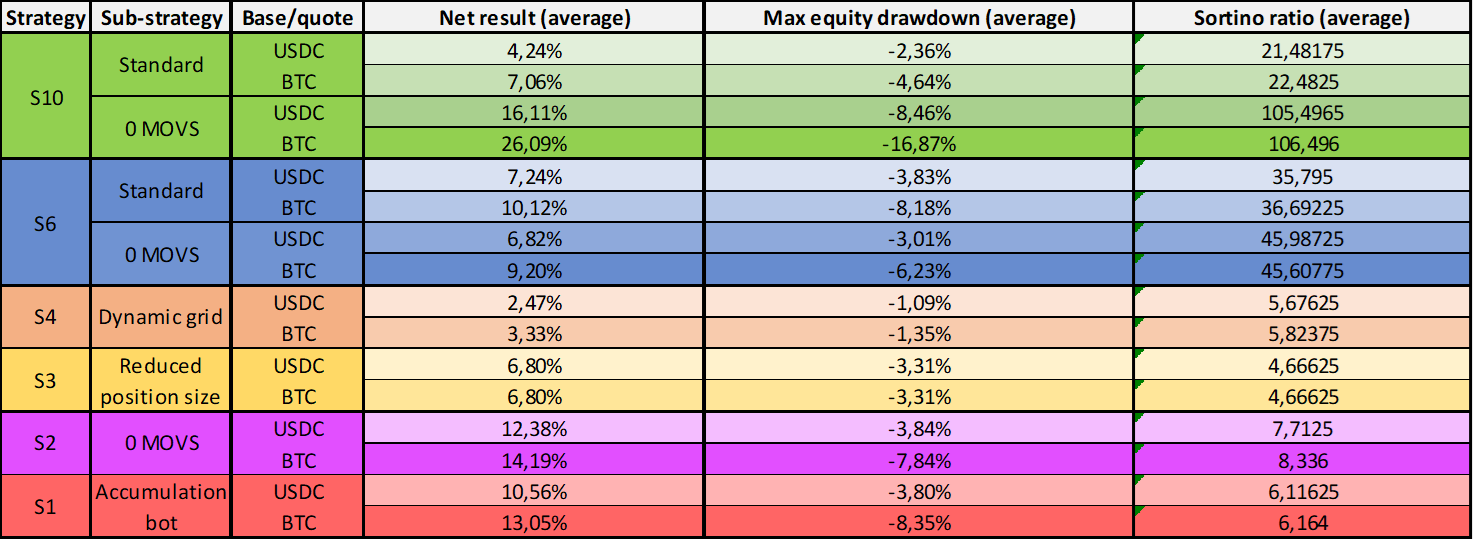

Here in this first table you can find the average results of the net profit, the drawdown and the sortino ratio for each backtest

No matter the strategy, if we profit in BTC the results are better. This is something we could have expected as the backtested period is during a bull run, so BTC is improving his value over time. Beware of a bear period the tendency could be the opposite.

The better the net profit, the worse the drawdown. No profits without risks.

0 MOVS seem to have better results than Standard strategies

The sortino ratio keeps getting better as long as the number of the S strategy gets bigger. Best strategy seems to be the S10 followed by the S6 in terms of Sortino ratio

3. Discussion:

Something it may worth be explained here is that when the net results/drawdowns are light (like in the S3 and S4 strategies), the main reason is because few trades have been made because the grids have been exceeded. Of course, there is the possibility to still open trades when grids are exceeded but other strategies seem more resilient to this phenomenon (S10 – S6), and this makes them more attractive to me. Another thing that could have been done is to reduce the backtesting period to a month instead of 3 months each time to try to reduce the exceeded grids but the backtesting would have taken ages.

Could be interesting to see if a compounding strategy would have let to better results. It’s something to test and that I started last time here (S-10) DCA by Simultaneous Deals

4. Conclusion:

After hours of backtesting, this only kind of demonstrates that @Rossano best strategies are the most recent ones, so this is nice because it shows that you are doing good work and we can only hope (or try to help at least) that it will be getting better and better.

I will update the tables with the new S Strategies backtested on the same periods when @Rossano will release them in order to have a fair comparison.

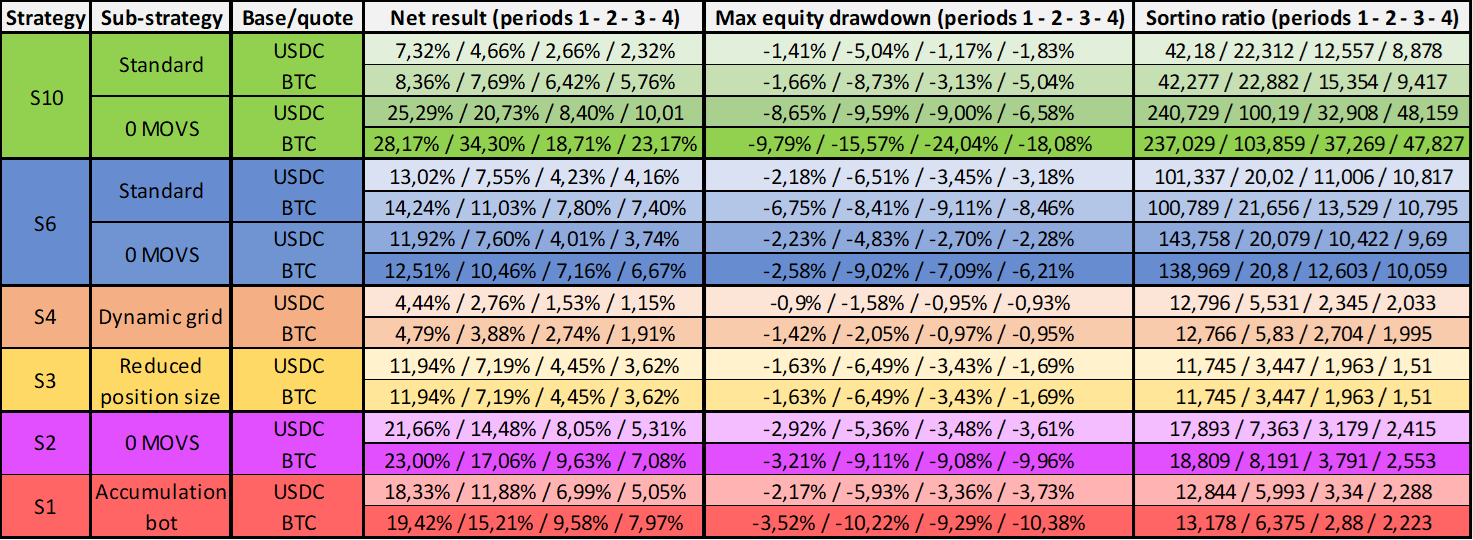

You can have a detailed view of the last table with all the results (not the average) in the next hidden word

What a job mate, really appreciate your effort and collaboration on these strategies - I will read through and give you any feedback and some insights I had in the past days

Trading should be a community effort not a SOLO run

Thank you so much for the thorough analysis, that’s great info!

One thing we need to consider about grids in general, but specially true when it comes to small grid step (like 0 movs) is that there will be candles that could go through several grids at once even in 1m candles. In those scenarios we don’t have intra candle movement and the backtest won’t be as accurate. In general, the higher the grid step, the less likely that a single 1m candle will span more than 1, and the more accurate it will be. That’s why paper trading is another important component of strategy testing, where you can check the strategy with tick by tick data.

The S-10 is still under development as I’m fixing little things I noticed while running the bots on a real account - NOTE the S-10 Standard hasn’t closed even a deal so it will be replaced by a better version which I’m working on already.

I suggested to run shorter backtests mainly because the risk management is embedded into each strategies - means if the market crash we can always do 3 things (stop, add funds/open new deals, wait).

The reason why the S-10 is developed on a trading bot rather than a combo bot is because the risk can be managed dynamically by merging the deals - this means that if the market experience a wider drawdown we can average the price of our deals by merging the deals - this means not extra funds and not hanging deals.

The 0 MOVS strategies work when we don’t pay any fees (0 fees pairings) if we then move on to a 0.07 fee pairing for example I wold suggest not less than 0.5-1% which means slower results

You are right when you say that

This is the main reason why we use two longs profiting in BASE and QUOTE - if the market is down our QUOTE stay the same while the BASE decrease in value and when the market is up our BASE increase in value while the QUOTE stay the same.

NOTE: when we profit from small movements we don’t need to use short bots - why? because we are profiting in BASE by follow every price movements - this means that we get free BASE at any price

An AUTO-compound strategy has been developed (S-5) but it doesn’t act as I thought since it doesn’t compound the profit made by the bots

I will add more feedback when I have new insights

Thanks again really appreciate your effort in looking at these strategies and spending time on them for the community interest

The S-6 has a lot of potential since I’m also adding manual deals which close in a few min/hours - this means that it can handle overlapping deals but it need a valid condition for all different scenarios otherwise we will increase the risk while increasing the usage of funds

@Perez Would you be happy to add 4 measures in your backtest for quick analysis and comparison overview? so every strategy has a score (1 to 5) for each aspect and a chart showing the main strategy features

FUNDS / BUDGET

RISK / EXPOSURE

PROFIT / COMPOUND

SPEED / PICKUP

Happy to collaborate on the google doc if you are ok in sharing the link